Most Indian option traders start by betting on direction — hoping Nifty goes up or Bank Nifty falls. But what if you could profit from pure market movement, regardless of the direction? That is what straddles and strangles are for. These classic non-directional setups allow you to trade the size of an expected price move rather than its path. They are the ultimate tools for trading high-impact events like corporate earnings announcements, monetary policy decisions, or union budget days. However, trading the straddle and strangle option strategy requires a clear grasp of implied volatility, time decay, and margin management, especially in the volatile Indian F&O space. Let’s break down how they work.

Nifty and Bank Nifty Option Chain analysis is critical here. Most option trades are bets on direction — up or down. Straddles and strangles are different: they’re bets on how much price moves, regardless of which way. That makes them the go-to structures for trading volatility, events and expiry. They’re also where many traders first get burned, so it pays to understand them properly.

The building blocks

Both strategies combine a call and a put on the same underlying and expiry. The difference is the strikes:

- Straddle — call and put at the same strike, usually at-the-money (ATM).

- Strangle — call and put at different strikes, typically an out-of-the-money (OTM) call and an OTM put.

And each can be long (you buy both) or short (you write both):

| Long | Short | |

|---|---|---|

| Straddle | Buy ATM call + ATM put | Sell ATM call + ATM put |

| Strangle | Buy OTM call + OTM put | Sell OTM call + OTM put |

Long straddle / strangle — betting on a big move

When you buy a straddle or strangle, you profit if the underlying makes a large move in either direction (or if implied volatility rises). You don’t care which way — you just need movement.

- Long straddle: maximum cost, but starts responding to a move immediately because it’s ATM.

- Long strangle: cheaper (OTM options cost less), but needs a bigger move before the OTM legs pay off.

The catch: your enemies are time decay and IV crush. Every day that price sits still, both legs bleed value. And if you buy before an event when IV is already high, the post-event IV collapse can sink you even if price moves your way. Long volatility works best when IV is low and a catalyst is genuinely underpriced.

A handy shortcut: the price of the ATM straddle ≈ the move the market is expecting by expiry. If the NIFTY ATM straddle costs 200 points, the market is roughly pricing a ±200-point move. To profit on a long straddle, price has to move more than that.

Short straddle / strangle — betting on a range

When you write a straddle or strangle, you collect premium up front and profit if the underlying stays range-bound (and/or if IV falls). Time decay is now your friend — every quiet day, the options you sold lose value and you keep more of the premium.

- Short straddle: richest premium, tightest profit zone (centred on the strike).

- Short strangle: lower premium, but a wider profit zone between the two OTM strikes — more breathing room.

The catch — and it’s a big one: short straddles and strangles have large, theoretically unlimited risk. A sharp move blows past your strikes and losses mount fast (this is “gamma risk,” and it’s brutal near expiry). These are advanced structures that demand strict position sizing, defined stops or protective wings (turning them into defined-risk “iron” variants). Never write naked volatility without a risk plan.

Choosing strikes and expiry

Implementing a successful straddle and strangle option strategy requires a solid trading plan. Unlike simple directional buying, non-directional option trading requires you to constantly monitor Greek risk—specifically Theta (time decay) and Vega (volatility sensitivity). For retail traders in India, understanding margin dynamics is also vital.

According to the margin guidelines laid down by the Securities and Exchange Board of India (SEBI), selling naked options requires substantial margin capital. While buying a straddle or strangle only requires the premium paid, writing them forces you to block significant margin, which can fluctuate wildly if market volatility spikes.

To optimize your margin efficiency when deploying a short straddle and strangle option strategy, many traders use “hedged wings.” By purchasing deep OTM options on both ends, you transform an unlimited-risk short strangle into a defined-risk Iron Condor. This not only caps your maximum loss but also drastically reduces the margin required by your broker.

Why IV crush matters

One of the most common pitfalls for beginners trading the straddle and strangle option strategy is ignoring Implied Volatility (IV). Before a major event, such as the Indian Union Budget or corporate earnings for heavyweights like Reliance or TCS, option premiums swell because of rising uncertainty. This means the IV is high, and the options are expensive.

As soon as the news is announced, the uncertainty vanishes. This leads to an immediate drop in IV, commonly referred to as “IV crush.” If you bought a long straddle or strangle before the announcement, the collapse in premium due to IV crush can easily wipe out any profits made from the actual price movement.

Thus, a long straddle and strangle option strategy is best initiated when IV is historically low, and you expect a sudden spike in volatility. Conversely, shorting volatility is highly profitable when IV is exceptionally high and expected to contract rapidly after the event.

Know your straddle and strangle breakevens

Before putting on a straddle or strangle, work out the breakevens — the points where the trade turns profitable. For a long straddle, that’s roughly the strike plus the total premium paid on the upside, and the strike minus the total premium on the downside. Price has to travel beyond one of those before expiry for you to make money. Mapping the breakevens up front keeps you honest about how big a move you actually need — and whether the market is already pricing it in via the ATM straddle.

When each straddle and strangle makes sense

- Expecting a big move (earnings surprise, breakout, event the market underprices), with IV low → long straddle/strangle.

- Expecting calm or a range, with IV high (rich premium to harvest) → short straddle/strangle, with risk controls.

- Unsure of direction but sure something will happen → long volatility, sized for time decay.

This is why implied volatility is inseparable from these trades: you’re really trading volatility, and the entry IV decides whether the structure is cheap or expensive. Short premium strategies are also a staple of expiry-day trading, where time decay is fastest.

Reading the chain for straddle and strangle trades

Use the Nifty and Bank Nifty Option Chain to pick strikes and check liquidity (tight bid-ask on both legs matters — you’re trading two options), and use open interest support and resistance to judge whether a range is likely to hold (helpful for short premium) or break (helpful for long premium).

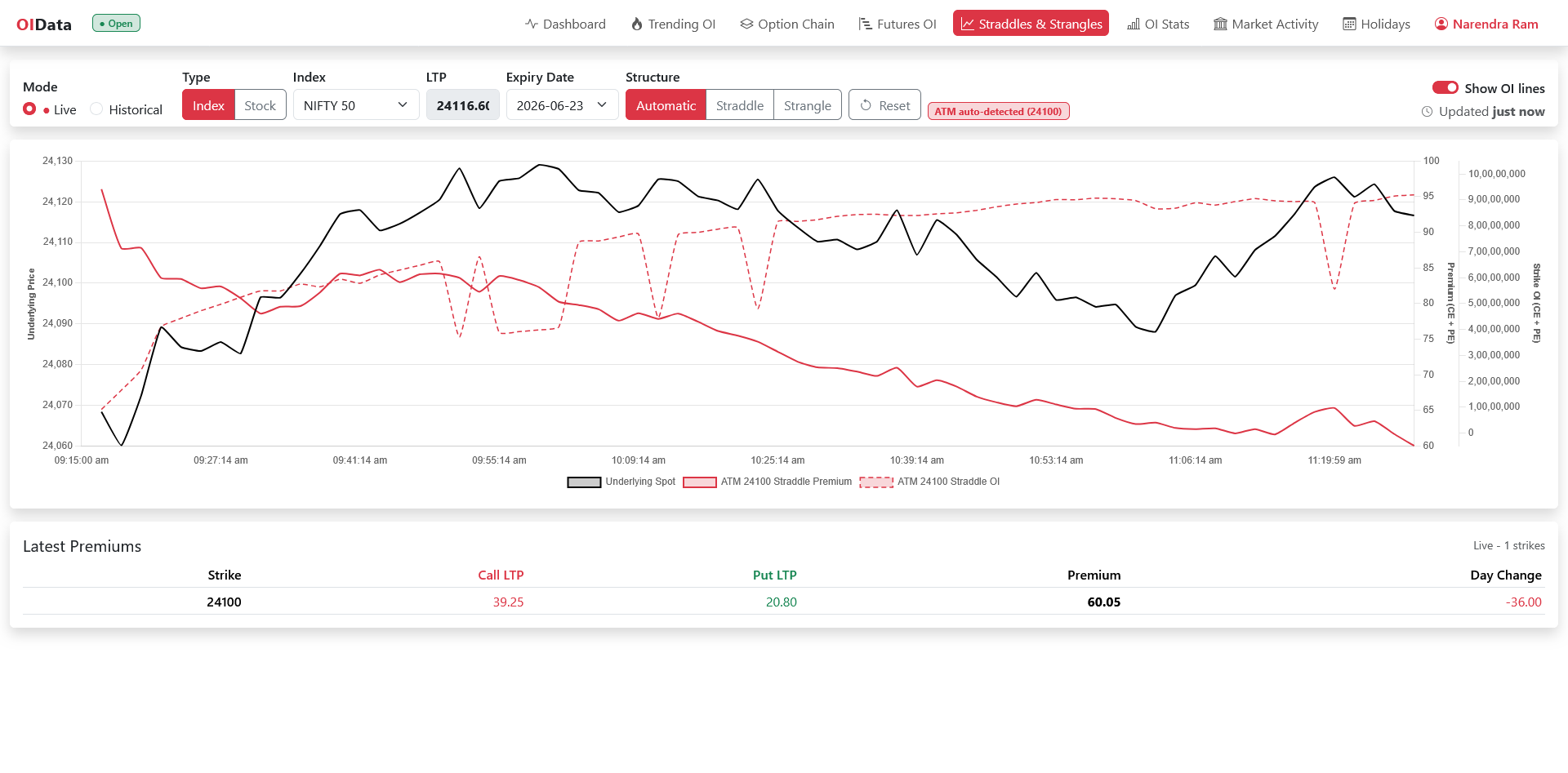

On OIData

The Straddles & Strangles page is built for these structures, and the Option Chain gives you the strike-level IV, OI and liquidity you need to set them up.

Related reading

The price of the at-the-money straddle is also the market’s own forecast of how far the index will travel — see expected move, which is computed from exactly the straddle and strangle premiums this article prices.

Takeaways

- Straddles and strangles let you trade the size of a move, not its direction.

- Straddle = same strike (ATM); strangle = different (OTM) strikes — cheaper but needs a bigger move.

- Long = bet on a big move / rising IV; enemies are time decay and IV crush.

- Short = bet on a range / falling IV; time decay helps but risk is large/unlimited — always use risk controls and monitor margins.

- The ATM straddle price ≈ the move the market expects; you need more than that to profit long.Open InterestOpen InterestOpen Interest